Award-winning PDF software

Irs tax 2555 for 2025 Form: What You Should Know

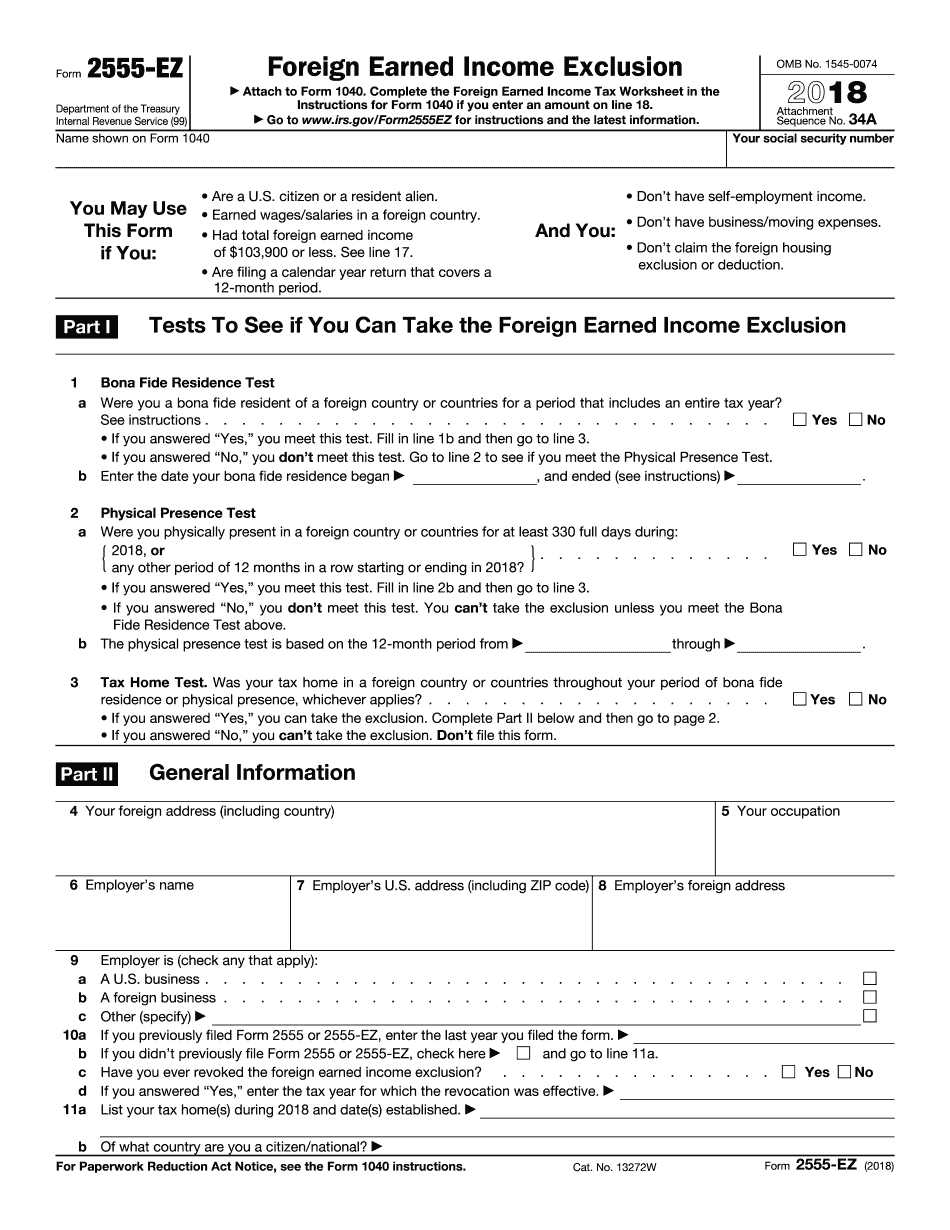

Unlike U.S. citizens living outside the United States, however, you have the additional benefits of U.S. taxation that most foreign residents do not enjoy. In general, you pay only a single regular income tax, no matter how long you live abroad. This is true even if you are subject to the alternative minimum tax. You do not have to use the foreign earned income exclusion (FIE) to claim the foreign tax credit or tax treaty discount on your U.S. income. Some additional information will help inform your 2025 foreign earned income tax information for Form 2555. For details, see Publication 519, Foreign Tax Credit. 1. How do foreign residents and U.S. citizens split income when they file Form 2555? Foreign Residents U.S. Citizens or Resident Aliens Form 2555, Foreign Earned Income, is a general tax information booklet. It does not have particular information for foreign residents, who have other ways to report their worldwide income or foreign earned income. Foreign residents should consult Form 2555-EZ, Foreign Earned Income Exclusion, for detailed information about the foreign earned income exclusion. In addition, if you are not a U.S. citizen or a U.S. resident alien, you should consult IRS Publication 515, Tax Guide for Americans Abroad, for details about U.S. tax issues that are specific to American citizens living abroad. Form 2555 includes instructions on how to fill in and file a completed form. 1. What is Form 2555-EZ? Form 2555, Foreign Earned Income Exclusion, (see below) is also known as the foreign earned income exclusion. Form 2555-EZ provides a foreign earned income exclusion that increases the exclusion from taxable income of individuals who are residents of a foreign country. U.S. taxpayers living in non-taxable countries, but who are U.S. citizens, can exclude up to 100,000 per beneficiary. Foreign-earned income for U.S. individuals living abroad is excluded from their taxable income for the 2025 tax year. Under current U.S. law, U.S. citizens are generally subject to a flat 10% tax on all income, whether it comes from U.S. sources, outside the U.S. or from sources within the United States; and only after an income tax is computed will a U.S. taxpayer find that amount is excluded from their income.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 2555-EZ, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 2555-EZ online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 2555-EZ by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 2555-EZ from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.