Award-winning PDF software

Form 2555-ez foreign earned income exclusion - internal

An income from sources within the United States (within the meaning of Section 902(a) (7)(A)-(C)). • Received any other type of exemption from tax imposed by this chapter. How to Use This Form If you, the spouse or dependent of an individual who has worked outside the United States, was a United States citizen or resident alien as of the close of the taxable year (December 31, close of the calendar year, for the current year, or a later date the IRS provides) and was paid more than the minimum remuneration (as defined in IRC Section 902(a) (7)(A)-(B)) for services rendered for an employer: 2. Identify the source salary of the nonresident alien. 3. Under section 6312, provide a statement to the IRS that the income from sources within the United States (as defined in section 902(a) (7)(A)-(C)) did not satisfy the requirements of the tax. If the income.

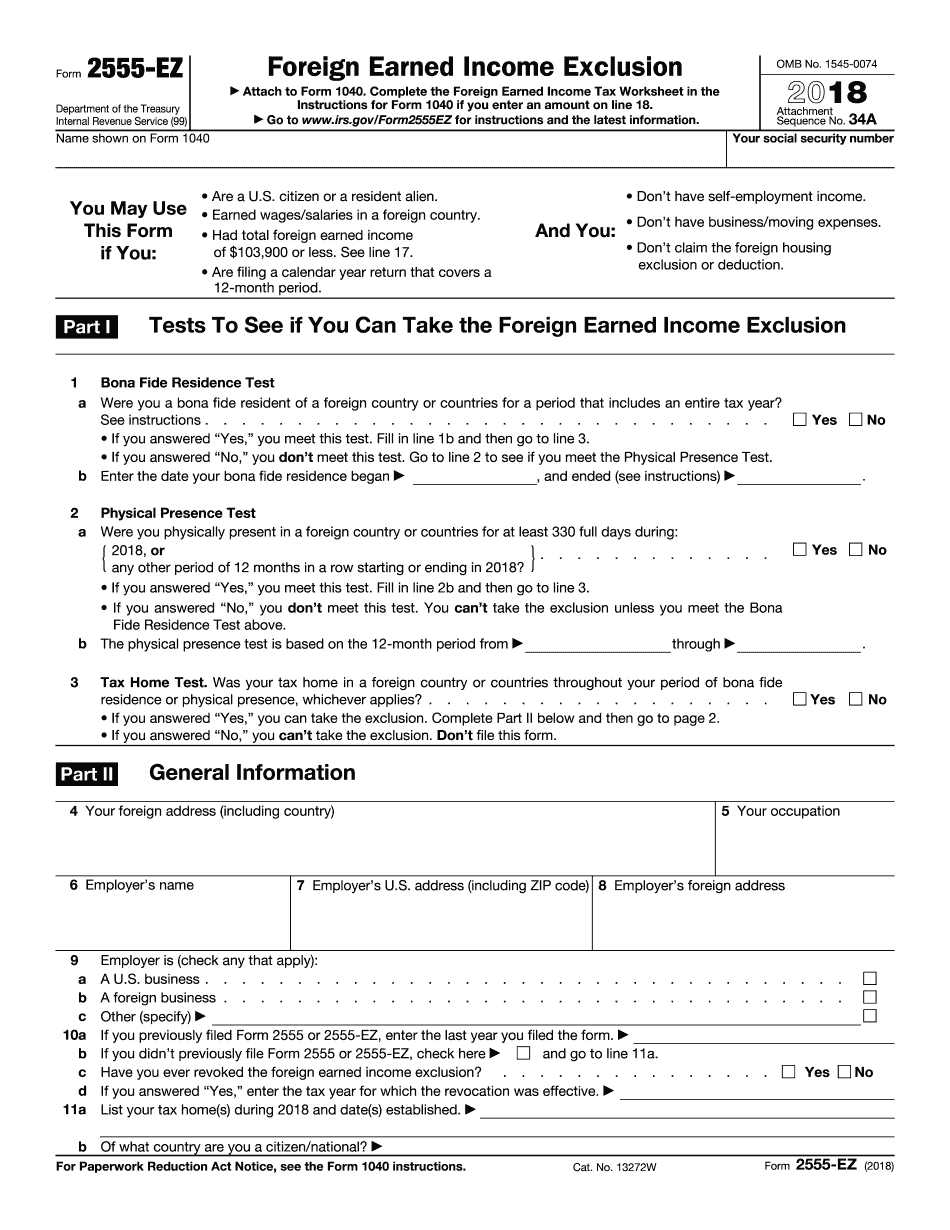

Foreign earned income exclusion: understanding form 2555

Form 2555-EZ: 2017 Changes Form 2555-EZ 2016 Changes Form 2555-EZ 2015 Changes Form 1040(X) (2) Form 1040(X) (1) Form : Tax Information 2016 Form 1040-EZ(1) : Form 1040(X) (2) Form : Electronic version of Form 1040 Form 2555-UZO : Form 2555-UZO provides information on the Federal Emergency Management Agency's (FEMA) requirements for an Individual Exemption. (This document has not been revised since it was released.) Form 2555-UZO : An Individual Exemption Form 2555-UZO: 2017 changes Form 2555-UZO 2016 changes Form 2555-UZO 2015 changes Form 2555-UZO 2014 changes Form 2555-UZO 2013 changes Form 2555-UZO 2012 changes Form 2555-UZO 2011 changes Form 2555-UZO 2010 changes Form 2555-UZO 2009 changes Form 2555-UZO 2008 changes Form 2555-UZO 2007 changes Form 2555-UZO : An Individual Exemption Form 2555-UP : Form 2555-UP provides information on the Federal Emergency Management Agency's (FEMA) requirements for an Individual Relief Act Exemption. (This document has not been revised since it was released.) Form 2555-UP : An Individual Relief Act Exemption Form : Electronic version of Form 2555-UP Form 2555-UZ: Form 2555-UZ is.

Form 2555-ez: us expat taxes

PDF filing penalties. They're also .pdf exempt from the Federal Form 1040 form as well. You can download Form 2555-EZ for free from the IRS website here. The form includes a page by page chart of the most common deductions, standard itemized deductions, and tax credits. To learn more about all the tax and government forms you can use, read my post at . A tax credit can be a refund you get that goes to pay part of a tax bill. For individuals, there are some tax credits that can reduce your tax bill. In addition, you can get a tax deduction for paying more than one kind of tax. When you combine a tax credit and a tax deduction, you can come out better off. Taxpayers can use the tax credits to reduce one kind of tax, while using the tax deductions to reduce another kind of tax, or.

Form 2555: how to claim the foreign earned income exclusion

Percent Medicare tax that's applied to most people over the age of 65. Form 2555 is a form filed for tax purposes only. You can't claim it on your personal US tax return. You can only claim it on your resident visa application. In this article, I'll go through the basics of the 2555, including what to expect, what to list on the form, and what to check when you file, according to the instructions. What is the 2555? The 2555 is a form you file with your native country (Italy) to claim the federal tax liability on your taxes owed there. You must file as a nonresident if you're not working (and you must be earning more than 100,000 a year in Italy as a nonresident). Because the 2555 is intended for US residents only, it's not a tax form that you used to claim any part of your social security benefits, Medicare.

What are forms 2555 and 2555-ez used for?

You have to file Form 2555 by February 1 of the year you want to treat the income in the most favorable way (including if you claim the foreign earned income or foreign housing exclusion, you have to file by April 15 of the first year you plan to exclude the income). The following are some examples for foreign earned income: You're citizen, resident or an alien who's living in the United States and have a home (or both) and other sources of income that exceed your source income: You have 250,000 in other sources of income. (This is a maximum of your foreign earned income, other source income and source income above 250,000. You must have total income above 250,000 in the year and still be a citizen, resident or an alien in the United States or other possession to be able to exclude 250,000 from domestic sources.) If.