Award-winning PDF software

NY Form 2555-EZ: What You Should Know

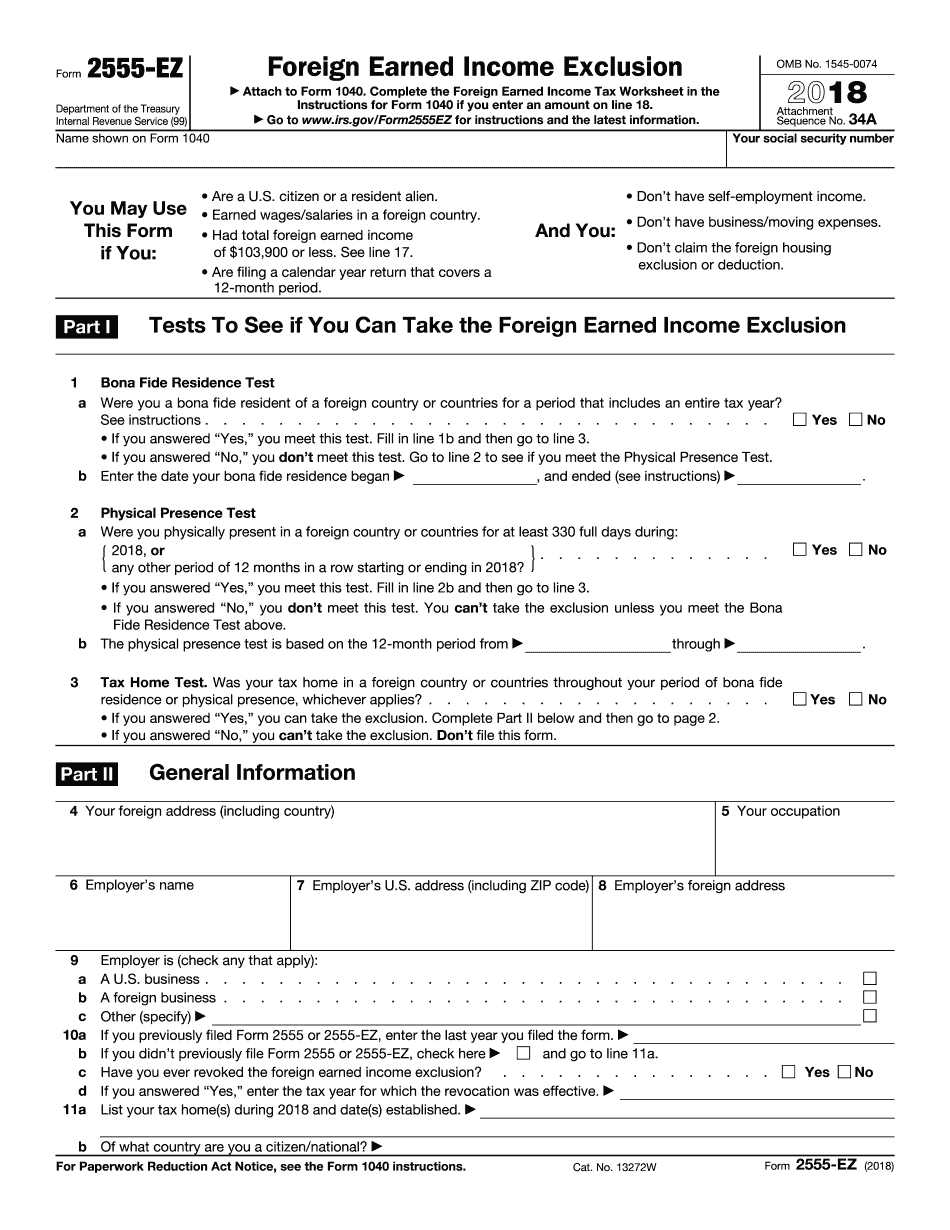

For 2018, these categories of income are not allowed as an offset against foreign taxes on the earned income. These are special taxes that apply to foreign earned income. The following types of taxes can still be claimed: The exclusion from income for dependent children of U.S. citizens, residents, and nationals. A charitable contribution deduction on a foreign tax return Qualified real estate losses If you have not taken the deductions above, it is still possible to minimize your foreign tax liability by taking all the appropriate deductions on the return and claiming the maximum allowable credits that you can on your tax return. What are Qualified Deductions and Qualified Real Estate Losses? To qualify for certain credits or deductions for the year, you had to own or lease property, either permanently (through your individual retirement account (IRA)) or temporarily, in the United States. If you were a resident of the United States only for part of the year (such as through a part-time foreign work leave), you may have to deduct a certain part or all of the qualified real estate losses from your U.S. tax and credits. The table below shows the maximum credit you can take for your qualified U.S. real estate losses. Credits by Month If you were a resident of the United States for only part of the year, you cannot deduct a loss on the income column, but it is possible to deduct a loss from the expenses' column. The deductions are based on what the loss is for, and the amount you can deduct is based on the total losses for your entire tax year. You can take a total deduction on your U.S. tax return of 100 from each of the qualified real estate losses for your entire tax year. Each loss on your income column that is in excess of either 10,000 (10,000 for married filing jointly) or 40% of the rental value of your home (if any) for the tax year must be subtracted from your net income on the Schedule A, Part II. The real estate loss allowed by the following rules may be deducted in full: The deduction is limited to 10% of the cost of your home, or 20% of the total qualified property gains on qualifying real estate. The deduction is limited to 10,000 for real estate lost on the casualty or theft of home property.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete NY Form 2555-EZ, keep away from glitches and furnish it inside a timely method:

How to complete a NY Form 2555-EZ?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your NY Form 2555-EZ aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your NY Form 2555-EZ from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.